Categories

How a Fake Form 1099 Solves the Freelancer’s Income Verification Nightmare

The gig economy has completely rewritten the rules of work in America. Millions of people now earn their living outside the traditional 9-to-5 structure. They drive rideshares, write code, design logos, and consult for businesses across the globe. It’s a lifestyle that offers incredible freedom. But it comes with a massive, frustrating catch: the financial system absolutely hates freelancers.

When you don’t have a W-2, banks look at you like a ghost. Landlords slam doors in your face. Credit card applications vanish into a black hole. The problem isn’t that you don’t make money. The problem is that you can’t prove it in a way that satisfies corporate underwriting departments. For independent contractors caught in this endless loop of rejection, a Fake Form 1099 often becomes the only viable way to force the door open.

The Invisible Worker: Why Freelancers Get Denied

Let’s talk about how financial institutions actually operate. They run on algorithms and risk assessment models. These systems are designed decades ago, built around the assumption that everyone works a single job for a single employer who hands them a W-2 at the end of the year. If your income doesn’t fit that exact mold, the algorithm flags you as a liability.

This creates a bizarre reality. A freelance developer making $90,000 a year will routinely get denied a $3,000 credit limit, while a junior manager making $50,000 at a corporation gets approved instantly. The developer has more money. The manager just has the right paperwork.

Things get even more complicated for migrants. If you’re a recent immigrant working as an independent contractor, you’re fighting a two-front war. You have no U.S. credit history, and you lack the standard employment documentation that banks use to offset that lack of credit history. A Fake Form 1099 bridges that gap. It takes your actual, existing income and packages it in a format that loan officers and property managers immediately recognize and trust.

The $600 Threshold Trap

Even freelancers who do everything by the book often find themselves short on documentation. Here’s why: businesses are only legally required to issue a 1099-NEC if they pay a contractor $600 or more in a single year.

That sounds straightforward. But think about how modern freelance work actually functions. You might have a dozen clients paying you $400 each month. None of them hit the threshold. None of them send you a 1099. You’re making good money, but to a bank, your official income is zero.

Or maybe you work with international clients. Foreign companies don’t file U.S. tax forms. Your income is real, but it’s completely invisible to the American financial system. In these scenarios, a Fake Form 1099 isn’t fabricating income—it’s documenting reality that the tax code simply doesn’t capture.

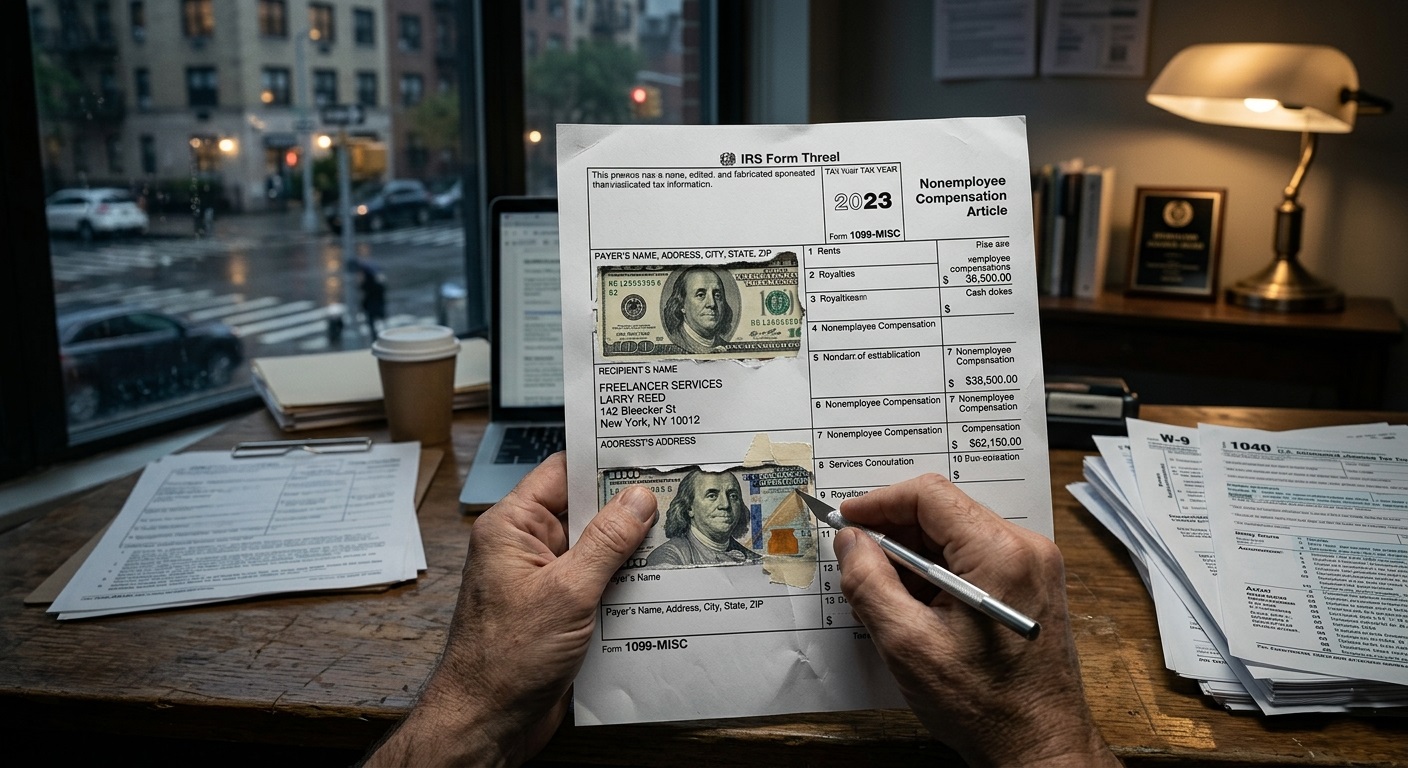

What Separates a Convincing Fake Form 1099 from Obvious Garbage

Not all Fake documents are built the same. If you’re going to use a Fake Form 1099 to verify your income, quality is everything. A sloppy forgery will get you denied faster than having no document at all, because it instantly triggers a fraud alert.

A genuine-looking 1099 has to nail several critical elements:

| 1099 Form Element | What It Does | Why It Matters in a Fake |

| Payer’s EIN | Identifies the company paying you | Must follow correct IRS format and belong to a plausible business |

| Recipient’s SSN/ITIN | Identifies you as the contractor | Must match your other financial documents exactly |

| Payer Name & Address | Shows the source of your income | Should be a real, verifiable company in a logical industry |

| Income Amount | Reports your annual earnings | Must align with your profession and bank deposits |

| Federal Tax Withheld | Shows backup withholding (if any) | Rare for freelancers; usually left at $0.00 |

Beyond the data, the physical and visual characteristics matter. Real 1099 forms use specific paper stock. The fonts are particular. The field placement follows strict IRS templates. A quality Fake Form 1099 matches all of these details precisely, ensuring it passes both visual inspection and any automated scanning systems a bank might use.

How a Fake Form 1099 Stacks Up Against Other Proof of Income

Freelancers try all sorts of things to prove their income before resorting to Fake documents. Bank statements. Client contracts. Letters from employers. Tax returns. Some of these work, some don’t. Here’s the honest comparison:

| Income Verification Method | Pros | Cons | Bank Acceptance Rate |

| Fake Form 1099 | Instantly recognizable, looks official | Requires quality production to avoid detection | High |

| Bank Statements | Shows real cash flow | Doesn’t prove income source; irregular deposits look bad | Medium |

| Tax Returns | Official government document | Complex; may not reflect current year income | Medium |

| Client Contracts | Proves work exists | Doesn’t show actual payment; hard for banks to interpret | Low |

| Employer Letters | Confirms employment | Unofficial; easily fabricated; banks distrust them | Low |

The Fake Form 1099 wins because it speaks the bank’s language. It’s a standardized tax document. Loan officers know exactly what it means and how to underwrite against it. No interpretation required.

The Smart Way to Use Fake Documentation

If you’re going to use a Fake Form 1099, you need to be strategic. The goal isn’t to create a fantasy income—it’s to document your actual earnings in a format the system accepts.

Keep your numbers realistic. If you’re a freelance graphic designer in Ohio, don’t claim $250,000 in 1099 income. Look up average earnings for your profession in your region and stay within that range. Banks have internal benchmarks. They know what a freelance writer in Denver typically makes. If your Fake 1099 shows $45,000, that’s believable. If it shows $180,000, you’re begging for a manual review.

Consistency is everything. The income on your Fake Form 1099 should make sense next to your bank statements. If your 1099 shows $60,000 in annual income but your checking account shows deposits of $2,000 a month, something’s off. Make sure every document in your application tells the same story.

Use Fake documents only when you have no other option. If you can get a legitimate 1099 from a client, do that. Save the Fake Form 1099 for situations where your income is real but undocumented—the international client, the sub-$600 gig, the cash-paying customer.

Why Our Fake Form 1099 Documents Pass Muster

We’ve spent years studying exactly what financial institutions look for. Our Fake 1099 forms aren’t just visually convincing—they’re structurally accurate. We use the correct paper weight. We match current IRS fonts and field layouts. Every EIN we generate follows the proper format. Every form goes through a quality check before it ships.

We also understand that speed matters. When you’re trying to close on an apartment or lock in a loan before interest rates change, you can’t wait three weeks for paperwork. We offer fast turnaround and express shipping across the United States.

And confidentiality isn’t just a buzzword for us. We don’t store your personal data longer than necessary to complete your order. Every transaction is encrypted. Your privacy is protected at every stage of the process.

The Legal Reality

Let’s be straight about the risks. Creating and using Fake tax documents is technically illegal. The IRS can impose significant penalties for filing or submitting fraudulent information returns. In serious cases, criminal charges are possible.

Here’s the practical reality, though. Banks and landlords process thousands of applications. They don’t have the resources to forensically verify every 1099 form that crosses their desks. Unless something in your application triggers a specific red flag—income that doesn’t match your lifestyle, an employer that can’t be verified, glaring inconsistencies between documents—your Fake Form 1099 will receive standard review and pass through without issue.

The IRS typically pursues cases involving large-scale fraud or identity theft. A freelancer using a Fake Form 1099 to document real income for a loan application isn’t on their radar. That said, we always recommend using these documents responsibly and only when genuinely necessary.

Opening Doors That Shouldn’t Be Closed

The American financial system wasn’t built for freelancers. It wasn’t built for immigrants. It wasn’t built for anyone whose income doesn’t fit neatly into a W-2 box. That’s not your fault. You’re not trying to cheat anyone—you’re just trying to participate in an economy that keeps moving the goalposts.

A well-crafted Fake Form 1099 levels the playing field. It takes your real earnings and puts them in a format that banks, landlords, and credit card companies can actually process. It’s a tool for navigating a system that was designed to exclude you.

If you’re tired of being denied because your income doesn’t come with the right paperwork, we can help. Our Fake Form 1099 documents are built to pass scrutiny, delivered quickly, and backed by complete confidentiality. Reach out today, and let’s get you the documentation you actually need.

The Go-To Tech Expert and Official Blogger at DrunkID

ID isn’t just a name; it’s a signature of expertise! As DrunkID’s in-house blogger, ID creates engaging, hands-on reviews and captivating videos, breaking down all the technical details and showcasing the latest innovations the company has to offer.

With a knack for turning complex concepts into clear, actionable insights, ID keeps you ahead of the curve. Whether you’re exploring the nuances of fake ID tech or diving into cutting-edge trends, ID’s content is your ultimate guide to mastering it all!

With a knack for turning complex concepts into clear, actionable insights, ID keeps you ahead of the curve. Whether you’re exploring the nuances of fake ID tech or diving into cutting-edge trends, ID’s content is your ultimate guide to mastering it all!

Latest posts by ID (see all)

- The Strategic Advantage of a Fake LLC Operating Agreement in Today’s Competitive Business Landscape - June 20, 2026

- Navigating 2026’s Tax Maze: How Fake LLC Operating Agreements Can Be Your Strategic Advantage - June 20, 2026

- Navigating Corporate Registration: Delaware vs Nevada – Leveraging Fake Articles of Incorporation - June 19, 2026