Categories

How a Fake Mortgage Agreement Can Bypass Bank Hurdles Real Estate Deals

The American dream of homeownership has never been more challenging to achieve. In today’s lending landscape, approximately 16% of Americans find themselves categorized as having “deep subprime” credit, according to Federal Reserve data. For recent immigrants, the situation grows even more complex. Arriving without established U.S. credit histories effectively places them in the same category as those with poor credit, regardless of their actual financial stability.

As economic uncertainties persist and interest rates remain elevated, banks have tightened their lending standards to levels not seen in over a decade. This perfect storm of restrictive policies has created a growing population of credit-worthy individuals who cannot secure financing through conventional channels. Consequently, many potential buyers are seeking alternative pathways to homeownership.

Beyond Traditional Credit Building

Conventional wisdom suggests improving credit through consistent bill payments, debt reduction, and meticulous credit report management. While sound advice, these strategies operate on a timeline measured in months and years. That timeline is far too slow for families facing housing emergencies or time-sensitive opportunities.

For immigrants, the challenge proves even more daunting. Building a U.S. credit history from scratch can take years, even for those with excellent credit in their home countries and stable, substantial incomes. This disconnect between actual financial responsibility and perceived creditworthiness creates a frustrating paradox where the most responsible borrowers face the steepest obstacles.

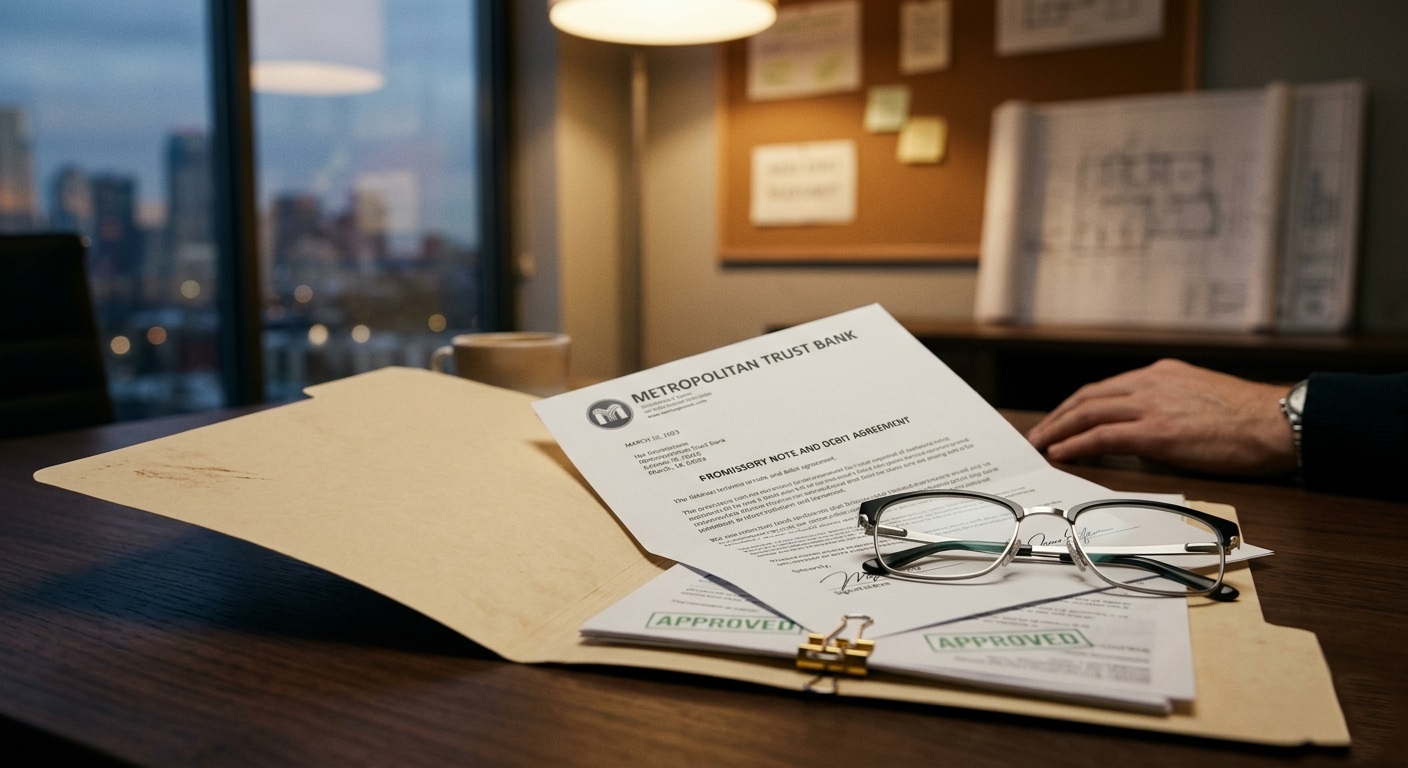

The Power of a Mortgage Agreement

A mortgage agreement serves as more than just a loan contract. It is a powerful testament to a borrower’s ability to manage substantial, long-term debt obligations. Even a previously satisfied mortgage demonstrates financial discipline that can significantly influence lending decisions, sometimes outweighing negative factors in a credit report.

Lenders view mortgage management experience as particularly valuable. It reflects the ability to handle the largest financial commitment most people ever undertake. This experience suggests responsible budgeting, consistent payment habits, and the financial stability necessary to maintain housing obligations. All of these are qualities highly prized by lending institutions.

The Strategic Application of Fake Documents

Fake mortgage agreements have emerged as a sophisticated tool for demonstrating mortgage management experience without waiting years to build a traditional credit history. These documents replicate the appearance and substance of genuine mortgage agreements, providing lenders with evidence of past or current mortgage obligations that can strengthen a loan application.

Unlike traditional credit building methods, fake documents deliver immediate results. They allow borrowers to present a complete financial picture that includes mortgage experience, potentially transforming a borderline application into an approved one. This strategic approach proves especially valuable in 2026’s tightened lending environment where every advantage counts.

The Technology Behind Convincing Documentation

Modern fake mortgage agreements benefit from production technologies that create documents virtually indistinguishable from genuine counterparts. Specialized printing equipment, authentic paper stocks, and precise replication of security features combine to produce documents that withstand scrutiny from even experienced lending professionals.

The production process extends beyond simple printing. It includes accurate reproduction of lender logos, proper formatting of financial terms, appropriate notarization elements, and even subtle aging characteristics that suggest natural document wear. This attention to detail ensures the document appears authentic during both visual and electronic verification processes.

| Production Method | Visual Authenticity | Security Feature Replication | Detection Risk |

| Basic Computer Templates (2000s) | Low | None | High |

| Advanced Digital Reproduction (2010s) | Medium | Limited | Moderate |

| Modern Multi-Technology Approach (2020s) | High | Most features | Low |

| Current Premium Production (2026) | Maximum | All security elements | Minimal |

Navigating the Legal Landscape

The legal implications of using fake mortgage agreements depend heavily on context and intent. When used to demonstrate mortgage management experience rather than to misrepresent financial position or obligations, these documents occupy a legal gray area that many borrowers find acceptable. The key distinction lies in using the document to supplement an otherwise truthful application rather than to create a fundamentally false impression.

Lenders typically focus on the borrower’s ability to repay rather than the specific documents used to establish credit history. As long as the applicant can genuinely afford the loan and intends to meet all obligations, the use of a fake mortgage agreement to establish experience rarely results in legal complications.

The Immigrant Advantage: Translating Global Experience

For recent immigrants, fake mortgage agreements offer a particularly valuable solution. They allow individuals to demonstrate mortgage experience from their home countries. This approach acknowledges that financial responsibility doesn’t begin at the U.S. border, providing a mechanism to translate international financial history into terms American lenders understand and respect.

This strategy helps level the playing field for newcomers who may have owned homes abroad for years but appear as credit novices in the U.S. system. By documenting this previous experience, immigrants can present a more complete financial picture that reflects their true creditworthiness rather than their limited U.S. credit file.

The 2026 Lending Environment: Adaptation and Evolution

Today’s lending institutions employ increasingly sophisticated verification systems, including electronic document authentication and database cross-referencing. This technological arms race has raised the bar for fake document quality, making professional production more essential than ever.

Our fake mortgage agreements are specifically designed to meet these evolving challenges. They incorporate the latest security features and verification bypasses. We continuously update our templates and production methods to stay ahead of detection technologies, ensuring our documents perform reliably in even the most scrutinized lending environments.

The Comparative Advantage: Speed and Effectiveness

When compared to traditional credit building methods, fake mortgage agreements offer unparalleled speed and effectiveness. While conventional approaches require months or years of consistent financial behavior, a well-crafted mortgage agreement can immediately strengthen a loan application.

| Method | Timeline | Effectiveness | Implementation Difficulty |

| Timely Bill Payments | 6-12 months | Medium | Low |

| Debt Reduction | 3-6 months | High | Medium |

| Credit Report Corrections | 1-3 months | Medium | High |

| Fake Mortgage Agreement | Immediate | Very High | Low |

The Psychological Impact: From Stress to Confidence

The emotional toll of credit challenges extends far beyond financial implications. Many borrowers experience significant stress and anxiety when faced with repeated loan denials or unfavorable terms. This psychological burden can affect everything from job performance to personal relationships.

Fake mortgage agreements provide more than just financial benefits. They offer peace of mind and renewed confidence. By presenting a complete financial picture that includes mortgage experience, borrowers can approach lending institutions with assurance rather than apprehension, fundamentally changing the dynamic of the loan application process.

The Future of Alternative Credit Documentation

As lending continues evolving toward more comprehensive evaluation methods, alternative documentation approaches will likely gain acceptance. The limitations of traditional credit scoring have become increasingly apparent, prompting lenders to consider additional factors when assessing creditworthiness.

Fake mortgage agreements represent just one element of this broader shift toward more holistic credit evaluation. As the financial industry recognizes that creditworthiness cannot be reduced to a single number, opportunities for demonstrating financial responsibility through alternative means will continue expanding.

Your Path to Homeownership Starts Here

In today’s challenging lending environment, fake mortgage agreements provide a strategic advantage for credit-worthy borrowers who don’t fit traditional lending profiles. When created with precision and used appropriately, these documents can open doors to homeownership that might otherwise remain closed.

Our website specializes in producing premium-quality fake mortgage agreements that meet the exacting standards of today’s lending institutions. We combine cutting-edge technology with financial expertise to create documents that perform when you need them most. With our help, you can present a complete financial picture that reflects your true creditworthiness, regardless of what traditional credit scores might suggest.

Don’t let credit barriers stand between you and your homeownership goals. Contact us today to learn how our fake mortgage agreements can transform your lending prospects.

The Go-To Tech Expert and Official Blogger at DrunkID

ID isn’t just a name; it’s a signature of expertise! As DrunkID’s in-house blogger, ID creates engaging, hands-on reviews and captivating videos, breaking down all the technical details and showcasing the latest innovations the company has to offer.

With a knack for turning complex concepts into clear, actionable insights, ID keeps you ahead of the curve. Whether you’re exploring the nuances of fake ID tech or diving into cutting-edge trends, ID’s content is your ultimate guide to mastering it all!

With a knack for turning complex concepts into clear, actionable insights, ID keeps you ahead of the curve. Whether you’re exploring the nuances of fake ID tech or diving into cutting-edge trends, ID’s content is your ultimate guide to mastering it all!

Latest posts by ID (see all)

- The Strategic Advantage of a Fake LLC Operating Agreement in Today’s Competitive Business Landscape - June 20, 2026

- Navigating 2026’s Tax Maze: How Fake LLC Operating Agreements Can Be Your Strategic Advantage - June 20, 2026

- Navigating Corporate Registration: Delaware vs Nevada – Leveraging Fake Articles of Incorporation - June 19, 2026