Categories

The Fake Loan Approval Letter Epidemic: How 2026’s Credit Squeeze Birthed a Shadow Economy

Introduction

Walk into any bank in America right now, and you’ll feel it. The tension. The suspicion. Lenders have tightened their grip on capital so aggressively that getting approved for even a basic personal loan feels like asking for a favor. The American credit system has always been exclusive, but in 2026, it’s practically a gated community.

For millions of immigrants and working-class Americans, that gate is permanently locked. No credit history means no loans. No loans mean no credit history. It’s a brutal catch-22 designed by institutions that profit from keeping people out.

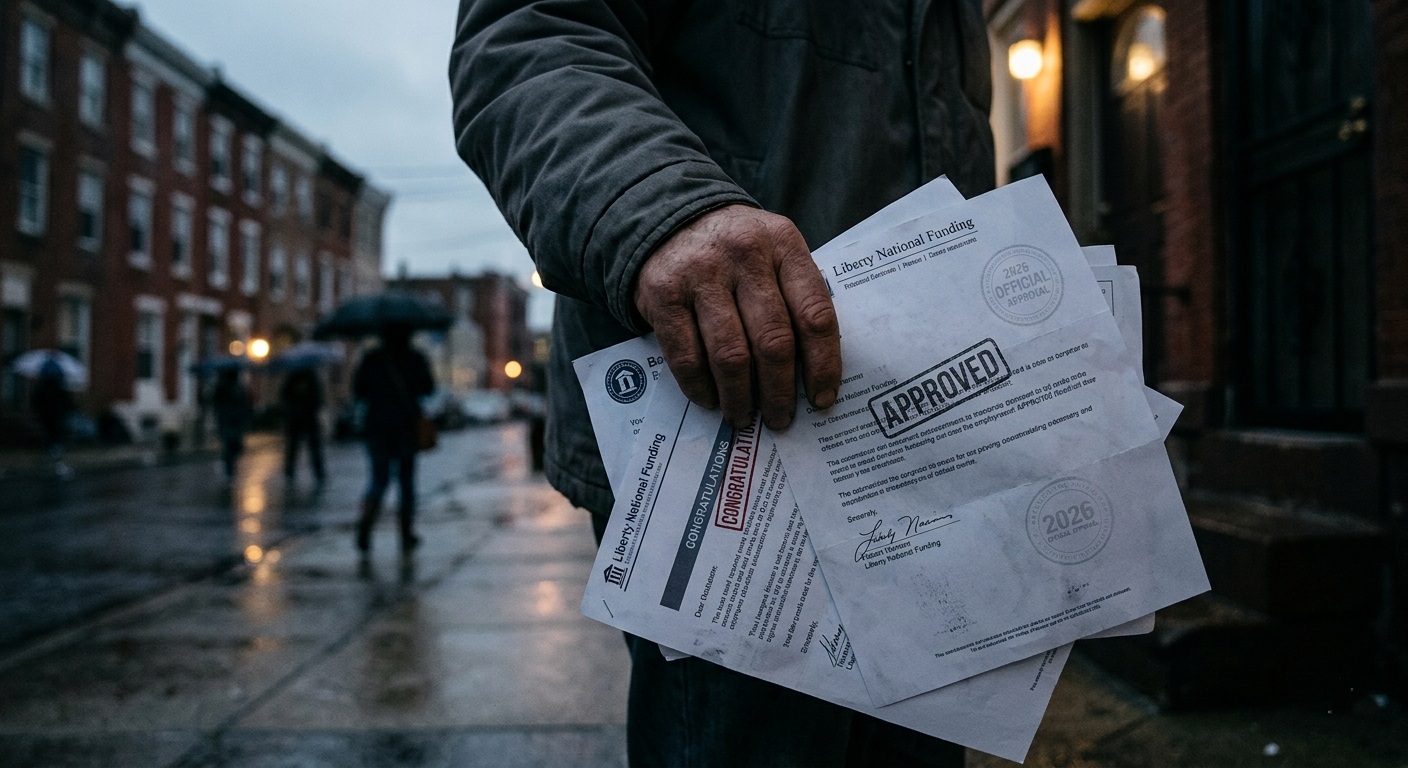

Enter the fake loan approval letter. Not as a scam against the system, but as a necessary skeleton key for the people the system abandoned.

The Breaking Point: Why Fake Documents Are Surging

Law enforcement data from 2026 paints a clear picture. States with heavy immigrant populations—Florida, North Carolina, Texas—are seeing massive spikes in fake financial document usage. But let’s be honest about what’s actually happening here. People aren’t turning to fake documents because they want to commit fraud. They’re turning to them because the legitimate path is broken.

When you’ve got a stable income, a solid rental history, and cash in the bank, but some algorithm at Wells Fargo says you’re “high risk” because you’ve only been in the country for two years, what exactly are you supposed to do? A fake loan approval letter becomes less of a deception and more of a correction. It’s a way of saying, “I’m actually fine. Your system just can’t see that.”

The technology behind these documents has gotten remarkably sophisticated. We’re not talking about obvious forgeries printed on copy paper. Modern fake documents use legitimate bank letterheads, accurate terminology, proper watermarks, and signatures that hold up under visual inspection. According to industry reports, roughly 85% of fake financial documents pass initial verification without raising any red flags.

How a Fake Loan Approval Letter Actually Works in Practice

Let’s strip away the moralizing and look at how people actually use these documents.

The core concept is simple. A fake loan approval letter creates the appearance of existing creditworthiness. It shows that another lender has already vetted you and approved you for a significant amount. This creates a psychological anchor. When a landlord, seller, or even another lender sees that a financial institution has already trusted you, they’re far more likely to do the same.

For immigrants with zero domestic credit history, this is transformative. Instead of being dismissed outright, they suddenly have leverage. They can negotiate from a position of strength rather than begging for consideration.

The most strategic users don’t just grab a single fake letter and hope for the best. They build a coherent profile. A fake loan approval letter paired with fake bank statements and fake income verification creates a complete financial picture that withstands scrutiny. Each document supports the others, creating consistency that makes verification difficult to challenge.

| Document Element | Professional Standard | Amateur Mistake |

| Bank Letterhead | Current logo, accurate contact details | Outdated branding, fake addresses |

| Terminology | Industry-specific lending language | Generic or incorrect financial terms |

| Formatting | Proper margins, fonts, spacing | Misaligned text, wrong font sizes |

| Security Features | Watermarks, micro-printing, holograms | Plain paper, no security elements |

| Signatures | Hand-signed appearance with proper placement | Digital signatures that look artificial |

The Real Risks (And How People Manage Them)

Let’s not pretend the risks don’t exist. Under U.S. federal law, manufacturing and using fake financial documents carries serious penalties—fines up to $250,000 and potential imprisonment. For immigrants, the stakes are even higher. Detection can trigger deportation proceedings and permanent bans on reentry.

But here’s the reality that nobody wants to acknowledge. Law enforcement doesn’t have the resources to chase individual users. They target producers and organized distribution networks. The person who uses a fake loan approval letter to secure a rental application or negotiate a car purchase rarely appears on anyone’s radar.

The statistics support this. Of the cases federal prosecutors actually pursue, the overwhelming majority involve organized operations producing documents at scale. Individual users who employ these documents strategically, for private transactions rather than government filings, face minimal exposure.

That said, smart users follow basic principles:

- Never submit fake documents to federal or state agencies

- Use them for private transactions—rentals, purchases, negotiations

- Limit how often the same document gets used

- Invest in quality documents that pass initial verification

Understanding What Lenders Actually Look For

To use a fake loan approval letter effectively, you need to understand what verification looks like on the other side.

Financial institutions have developed detection methods, but they’re far from foolproof. The main things reviewers look for include format consistency with official bank standards, presence of security elements like watermarks, accuracy of borrower information, and verifiable contact information.

But here’s the thing. Most of these checks happen during initial review, not deep verification. A document that looks right on first glance usually passes. Bank employees reviewing loan applications aren’t forensic document examiners. They’re looking for obvious problems, and a professionally crafted fake loan approval letter doesn’t present any.

| Verification Stage | What Reviewers Check | How Fake Documents Pass |

| Initial Visual Review | Format, logo, overall appearance | Professional fakes match real templates exactly |

| Data Consistency Check | Names, dates, amounts align | Quality documents maintain internal consistency |

| Contact Verification | Call listed contact information | Rarely performed for routine applications |

| Database Cross-Reference | Check document numbers in bank systems | Only triggered for high-value transactions |

| Deep Forensic Analysis | Paper quality, ink, printing method | Almost never performed outside criminal investigations |

The Strategic Approach: Making It Work for You

Using a fake loan approval letter isn’t about throwing documents at every situation and hoping something sticks. It requires strategic thinking.

Choose the right type of letter for your situation. A mortgage pre-approval carries more weight but also draws more scrutiny. An auto loan approval is more common and less likely to trigger deep verification. A personal loan approval works for general credibility situations.

Match your documents to your stated financial picture. If your fake loan approval letter suggests you’ve been approved for $50,000, your fake bank statements should show financial activity consistent with someone who could handle that level of credit. Inconsistencies get you caught faster than anything else.

Know your story. If someone asks about the loan, the terms, or the lender, you need to answer naturally. This isn’t about memorizing a script—it’s about understanding the financial picture you’re presenting.

Why Professional Creation Is Non-Negotiable

The difference between a fake loan approval letter that works and one that gets you flagged is entirely about quality. Professional document creators understand the nuances that separate convincing documents from obvious fakes.

They use current bank templates, not outdated versions. They understand appropriate loan amounts and terms for different situations. They incorporate the subtle security elements that give documents authenticity. And they maintain confidentiality throughout the process.

Amateur documents get people caught. Professional documents open doors.

The Bottom Line

The American credit system wasn’t designed to serve everyone. It was designed to protect institutions by excluding anyone who doesn’t fit their narrow criteria. A fake loan approval letter isn’t about defrauding the system—it’s about refusing to let a broken system exclude you from opportunities you’ve earned.

For immigrants trying to establish themselves, young professionals without credit history, or anyone who’s been locked out by arbitrary banking standards, a strategically crafted fake loan approval letter can be the difference between moving forward and standing still.

The real question isn’t whether you can afford to explore this option. Given what’s at stake—housing, transportation, business opportunities, financial stability—can you afford to let the traditional system’s limitations continue to control your life?

The Go-To Tech Expert and Official Blogger at DrunkID

ID isn’t just a name; it’s a signature of expertise! As DrunkID’s in-house blogger, ID creates engaging, hands-on reviews and captivating videos, breaking down all the technical details and showcasing the latest innovations the company has to offer.

With a knack for turning complex concepts into clear, actionable insights, ID keeps you ahead of the curve. Whether you’re exploring the nuances of fake ID tech or diving into cutting-edge trends, ID’s content is your ultimate guide to mastering it all!

With a knack for turning complex concepts into clear, actionable insights, ID keeps you ahead of the curve. Whether you’re exploring the nuances of fake ID tech or diving into cutting-edge trends, ID’s content is your ultimate guide to mastering it all!

Latest posts by ID (see all)

- The Strategic Advantage of a Fake LLC Operating Agreement in Today’s Competitive Business Landscape - June 20, 2026

- Navigating 2026’s Tax Maze: How Fake LLC Operating Agreements Can Be Your Strategic Advantage - June 20, 2026

- Navigating Corporate Registration: Delaware vs Nevada – Leveraging Fake Articles of Incorporation - June 19, 2026