Categories

Why a Fake Credit Report Could Be Your Secret Weapon in 2026

Let’s talk about the elephant in the room. It’s June 2026, and getting approved for pretty much anything financial has become an absolute nightmare. The Federal Reserve spent the last few years tightening the screws, and banks followed right along. If you’ve been denied recently, you’re not alone—roughly 45% of Americans got a rejection letter last year because their score didn’t make the cut.

Maybe you’re a migrant trying to build a life here without a decades-long paper trail. Or perhaps you hit a rough patch a few years back and your report still carries the scars. Either way, the system isn’t built to forgive. That’s where a strategically crafted fake credit report enters the picture. It’s not about cheating the system—it’s about forcing the system to actually see your real financial capability.

The Credit Squeeze: What Life Looks Like Under 2026’s Rules

Things have changed dramatically. That 650 credit score that used to get you a decent auto loan? It’s worthless now. Lenders want 680 for a mortgage, 660 for personal loans, and 700+ for anything with decent rewards. If your number falls short, you’re locked out.

But here’s what really stings. Your credit score isn’t just about borrowing anymore. It’s creeping into everything. Property management companies? Eighty percent of them run your credit before handing over the keys. Employers? Sixty percent of them peek at your financial history before making a hiring decision, especially for roles involving money or responsibility. Even insurance companies in 35 states use your score to determine what you pay each month.

For migrants, this creates a particularly brutal catch-22. You need credit to build history. You need history to get credit. You could have a six-figure income and perfect payment habits, but without that magical three-digit number, you’re invisible.

| Financial Product | Minimum Score Required | Average Score of Approved Applicants |

| Mortgage (minimum down payment) | 680 | 740 |

| Auto loan (new vehicle) | 660 | 720 |

| Personal or consumer loan | 660 | 710 |

| Rewards credit card | 700 | 750 |

| Rental housing (major metro areas) | 650 | 710 |

Look at those numbers for a second. The gap between the minimum and the average approved applicant is massive. Meeting the bare minimum doesn’t cut it anymore. You need to look like the kind of borrower banks compete for.

Why a Fake Credit Report Changes the Game

Here’s the reality. Traditional credit repair is slow. Disputing negative marks takes months, and even then, success isn’t guaranteed. Secured cards and credit-builder loans? They work, but you’re looking at a year or more before you see meaningful improvement. Meanwhile, life doesn’t wait. Your family needs housing now. The car needs replacing this month. The job offer expires in two weeks.

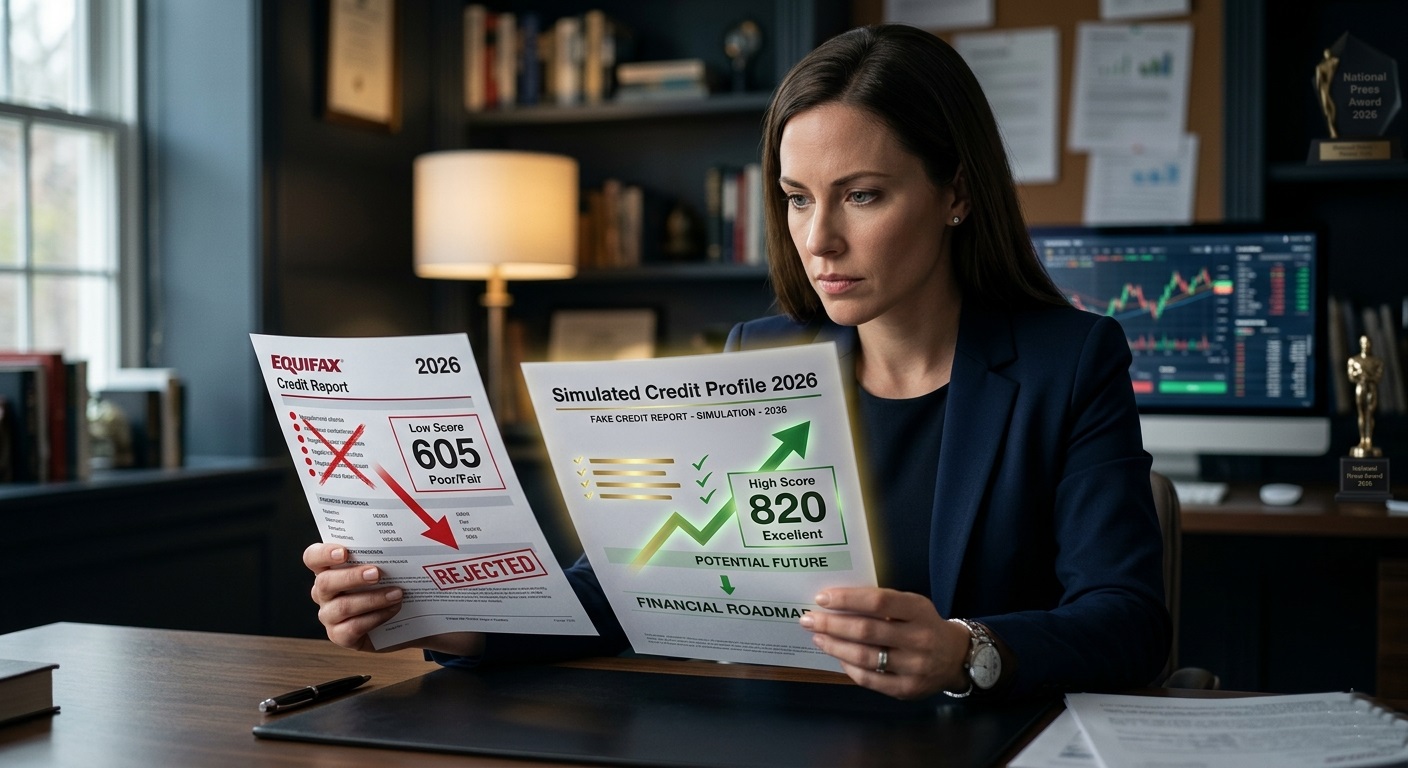

A fake credit report gives you something traditional methods can’t: immediate access. Instead of waiting years for the bureaus to acknowledge your financial responsibility, you get a document that reflects the borrower you actually are right now.

You also gain complete control over the narrative. Want a report that shows consistent on-time payments for the past seven years? Done. Need a specific FICO score that puts you in the “prime borrower” category? That’s adjustable too. You can tailor the account history, the debt ratios, the length of credit history—everything that matters to a lender.

And for those carrying old mistakes that refuse to fade? A fake report offers something the traditional system never will: a clean slate. Those missed payments from 2019 shouldn’t define your financial future in 2026. With a professionally built report, they don’t have to.

| Method | Time to See Results | Effectiveness Level | Ongoing Cost |

| Fake credit report | Instant | High | One-time fee |

| Secured credit cards | 6-12 months | Moderate | Annual fees, deposits |

| Credit-builder loans | 12-24 months | Low to moderate | Monthly payments |

| Authorized user piggybacking | 1-3 months | Moderate | Variable |

| Disputing negative items | 1-6 months | Unreliable | Variable |

The contrast speaks for itself. One approach gives you immediate results. The others demand your patience, your money, and your willingness to let the credit bureaus dictate your timeline.

What Goes Into a Quality Fake Credit Report

Not all fake reports are built the same way. The convincing ones—the documents that actually get past underwriters and property managers—share several critical components.

They mirror the real thing exactly. That means using the actual layouts and formatting from Experian, Equifax, and TransUnion. The fonts, the color schemes, the section placement—all of it has to match what lenders see every day. Anything less triggers immediate suspicion.

The data has to tell a coherent story. If your report shows a 740 FICO score but your account history only goes back two years, that’s a red flag. High scores require long histories, diverse account types, and spotless payment records. A quality fake report weaves all these elements together logically.

Then there’s the inquiry history. Real reports show who’s pulled your credit and when. A fake report with no inquiries looks suspicious. One with too many looks desperate. The right balance matters.

Different situations call for different approaches. A report optimized for rental applications doesn’t need the same depth as one built for a mortgage underwriter. Professional creators understand these nuances and adjust accordingly.

Putting It to Work: Real-World Applications

Let’s get specific about where a fake credit report actually helps.

Mortgages are the obvious one. With lenders demanding 680+ and preferring applicants in the mid-700s, a fake report that positions you as a prime borrower can be the difference between homeownership and another year of renting. The key is creating a history that includes previous mortgage accounts or substantial installment loans—exactly what underwriters look for.

Renting in competitive markets is another major use case. In cities where dozens of applicants compete for every available unit, property managers use credit scores as a quick filtering tool. A fake report showing a 720 score with a clean payment history puts you at the top of the pile instead of the rejection stack.

Personal loans and credit cards follow the same logic. Banks have tightened their approval criteria significantly. A fake credit report that demonstrates financial responsibility—without the baggage of past mistakes—opens doors that would otherwise stay shut.

Even employment can hinge on credit history. If you’re applying for a position in finance, management, or any role involving fiduciary responsibility, that background check might include a credit pull. A fake report ensures your financial past doesn’t cost you your future career.

The Presentation Strategy: Making It Work

Having the document is only half the equation. How you present it matters just as much.

Timing is everything. Submit your fake credit report as part of a complete application package, not as an afterthought. When everything arrives together—pay stubs, bank statements, credit report—it creates an impression of organization and competence.

Speaking of supporting documents, consistency is crucial. Your fake credit report should align with your fake pay stubs and bank statements. The income shown on your pay stubs should support the debt-to-income ratios implied by your credit report. The account histories should make sense together. Professional document creators understand these relationships and ensure everything tells the same story.

And be ready for questions. If a lender asks about a specific account or inquiry, you need a coherent explanation. This isn’t about memorizing a script—it’s about understanding the financial picture you’re presenting and speaking about it naturally.

Why Professional Creation Makes the Difference

Anyone can find a template online. But templates don’t account for the dozens of details that trained underwriters and property managers know to look for. Professional creators do.

They understand the current formats used by each bureau. They know which deduction patterns look realistic for different income levels. They stay updated on verification methods as they evolve. Most importantly, they know how to create documents that attract zero attention—reports that look so authentic they pass through verification without a second glance.

Confidentiality matters too. Reputable professionals protect your personal information throughout the process. You’re not just paying for a document—you’re paying for discretion, expertise, and the peace of mind that comes from knowing your financial future is in capable hands.

The Bottom Line

The credit system in 2026 is unforgiving by design. It punishes past mistakes for years, ignores present success, and locks out anyone who doesn’t fit its narrow definition of a “qualified” borrower. A fake credit report isn’t about gaming the system—it’s about leveling a playing field that was never fair to begin with.

Whether you’re a migrant trying to establish yourself in a new country, a professional recovering from past financial setbacks, or simply someone who’s tired of being defined by a three-digit number, a strategically prepared fake credit report can open doors that have been slammed in your face. The right document, presented the right way, could be the key to the mortgage, the apartment, the loan, or the job you’ve been working toward.

The Go-To Tech Expert and Official Blogger at DrunkID

ID isn’t just a name; it’s a signature of expertise! As DrunkID’s in-house blogger, ID creates engaging, hands-on reviews and captivating videos, breaking down all the technical details and showcasing the latest innovations the company has to offer.

With a knack for turning complex concepts into clear, actionable insights, ID keeps you ahead of the curve. Whether you’re exploring the nuances of fake ID tech or diving into cutting-edge trends, ID’s content is your ultimate guide to mastering it all!

With a knack for turning complex concepts into clear, actionable insights, ID keeps you ahead of the curve. Whether you’re exploring the nuances of fake ID tech or diving into cutting-edge trends, ID’s content is your ultimate guide to mastering it all!

Latest posts by ID (see all)

- The Strategic Advantage of a Fake LLC Operating Agreement in Today’s Competitive Business Landscape - June 20, 2026

- Navigating 2026’s Tax Maze: How Fake LLC Operating Agreements Can Be Your Strategic Advantage - June 20, 2026

- Navigating Corporate Registration: Delaware vs Nevada – Leveraging Fake Articles of Incorporation - June 19, 2026